Implementing the UK’s MRT pay reforms: what compensation leaders need to decide now and consider for tomorrow (and how to weigh accelerating legacy deferrals)

UK banks, investment firms and dual‑regulated firms operating in financial services are entering a new phase of remuneration reform. Following changes to the Financial Conduct Authority (FCA) and PRA Prudential Regulation Authority (PRA) remuneration rules, firms now have greater flexibility over variable remuneration, deferral periods, vesting and retention period structures, particularly for material risk takers and senior management functions. With the bonus cap removed and the new rules applying from the 2026 performance year, remuneration committees are being asked to revisit long‑standing assumptions about fixed pay, variable pay, total pay and the treatment of deferred awards and bonus awards, including the design of bonus deferral arrangements. At the same time, expectations around risk‑taking, individual accountability, proportionality and risk management remain firmly in place, including the treatment of risk events. This article explores what has changed under the PRA’s remuneration rules and the FCA rules, what discretion is genuinely available under the remuneration code and how remuneration committees can approach decisions on vesting, deferral and legacy deferred awards in a way that is defensible, proportionate and aligned with their firm’s risk profile.

The reform backdrop, what’s changed, what’s optional and what’s still expected

The context

Over the last two years, the UK regulators have reshaped the bank remuneration framework and overall remuneration regime to make it “more effective, simple and proportionate,” and to align risk and reward while improving UK competitiveness across financial services. Key changes include:

- the removal of the bonus cap

- simplification of MRT identification, including a shift away from purely quantitative criteria

- shorter, simpler deferral rules and retention expectations, including a shift away from purely quantitative criteria and a sharper focus on the high earners

- higher thresholds for heavier deferral

- streamlining of FCA rules to cross‑refer to the PRA regime and PRA rulebook, reducing regulatory duplication

Most measures apply mandatorily to performance years beginning after 16 October 2025 (i.e., 2026 for calendar‑year firms), with discretion to adopt some proposed changes sooner and even to unvested past awards, subject to governance and shareholder approval.

At‑a‑glance reforms

- Bonus cap removed (effective 31 October 2023): firms must instead set an “appropriate” fixed/variable ratio within the Code’s risk‑alignment tools (deferral, instruments, malus/clawback)

- MRT scope simplified: stronger governance around firm‑owned MRT identification, with focus on qualitative criteria and a “top 0.3% earners” consideration; fewer staff expected to be in scope relative to CRD‑era quantitative thresholds

- Deferral and vesting: a single minimum four‑year deferral for all MRTs (replacing 7–8 years for the most senior), pro‑rata vesting from year one for SMFs now permitted, no mandatory retention for deferred instruments (retention still expected for upfront instruments), and ability to pay dividends/interest on deferred instruments. Some elements may be adopted early, including for unvested legacy awards

- Heavy deferral threshold raised: the 60% deferral rate now applies above GPB 660,000, with 40% on the first GBP 660,000 (marginal application)

- FCA Handbook streamlined (SYSC 19D largely cross‑refers to PRA rules)

European Union lens (if you have EU entities)

The EU (under CRD V/VI and EBA Guidelines) retains a stricter model, bonus cap, de minimis proportionality rules, and four-to-five-year minimum deferrals, so UK‑group designs must still manage cross‑border inconsistencies and potential exemption differences across jurisdictions.

The decision facing Remuneration Committees now: accelerate vesting of historic deferred awards?

With shorter deferral allowances and more flexible vesting now available under the final rules, many RemCos are asking whether to accelerate vesting on legacy deferrals (awards from prior cycles still in the pipeline). The regulators have signalled that certain reforms may be applied to awards “not yet vested,” giving boards legal room to consider acceleration, subject to governance, malus, clawback periods and fairness.

Below are the principal arguments for and against acceleration, and how to balance them where role‑based allowances (RBAs) remain part of the pay mix for some MRTs.

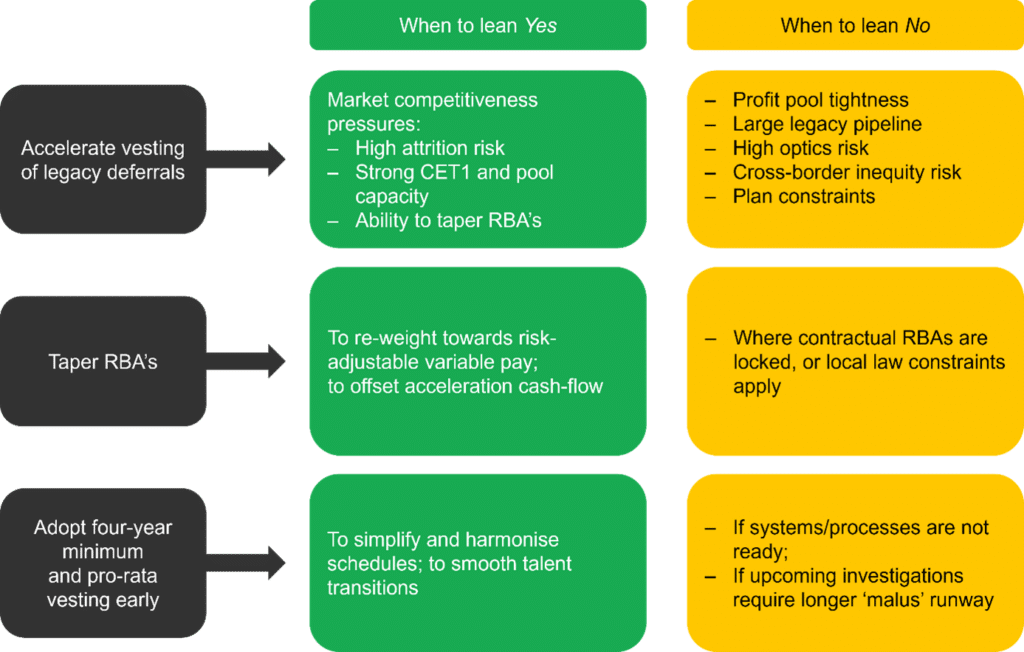

Arguments for accelerating vesting of legacy deferrals

- Strategic alignment with the new regime: if the policy goal is to pivot back toward variable pay (after the bonus cap drove fixed‑pay inflation through salaries and RBAs), allowing faster access to deferred variable pay, demonstrates realignment and may support competitiveness and recruitment/retention in global markets

- Employee value proposition and portability: senior hires increasingly benchmark to US/Asia structures with shorter deferral and more front‑loaded vesting. Early vesting (subject to malus/clawback) can make UK packages more comparable without expanding fixed pay

- Simplicity and administrative burden: fewer overlapping vesting schedules reduce complexity and compliance cost, an explicit aim of the reforms and FCA rulebook streamlining

- Risk alignment maintained: the core risk levers remain. They include malus, clawback (up to seven-to-ten years for senior roles in historical frameworks) and payment in instruments. Boards can keep robust triggers and extend hold‑through policies for upfront instruments to preserve alignment

Arguments against accelerating vesting

- Cost, liquidity and profit‑pool impact: large MRT populations imply large unvested “tails.” Accelerating vesting compresses cash/share outflows into near‑term periods, potentially reducing future‑year profit pools and straining CET1‑conscious funding envelopes (especially if the firm already increased fixed pay/RBAs during the cap era)

- Optics and conduct risk: public and supervisor scrutiny may intensify if acceleration appears to “enrich” bankers, particularly if performance is volatile. RemCos must evidence that changes do not weaken risk alignment and remain consistent with the firm’s risk appetite statements

- Cross‑border complexity: for groups with EU entities, accelerating UK awards while EU rules still demand longer deferral/bonus cap compliance can create internal inequity and mobility frictions

- Contractual and plan rule constraints: many legacy plans hard‑code vesting schedules or retention periods. Any modification must respect plan rules, shareholder‑approved terms, and listing/market abuse controls on discretionary changes. (Regulatory sources underscore governance and documentation standards, even as they allow discretion)

- Impact on buy‑out valuations and re‑notification duties: where former MRTs have moved to another employer and a Remuneration Statement has already been issued for buy‑out valuation, any later change to vesting structures, deferral periods or award values may require the firm to re‑notify the hiring employer. This introduces an additional administrative step, particularly if the revised terms materially alter the value of unvested awards previously relied upon

- Employment contract and incentive plan updates: employers will need to review contracts, plan rules, leaver provisions and deferral clauses to ensure alignment with the new regulatory framework. Updated minimum deferral or retention periods must be reflected in documentation so that future awards remain compliant and do not create misalignment or disputes for MRTs who leave

Strategic pacing and market positioning

Early adoption may improve competitiveness but risks administrative complexity and inconsistent treatment of legacy awards. Moving too slowly risks falling behind market practice as peers adopt shorter deferral models. While many firms may take a wait‑and‑see approach, they should still quantify the potential impact on buy‑outs, profit pools, cross‑border populations and risk governance before adjusting schedules.

The RBA question: balancing role‑based allowances with accelerated vesting

What RBAs are (and why they matter)

RBAs proliferated in the bonus‑cap era as quasi‑fixed pay to preserve total comp competitiveness. EBA guidance historically pushed firms to classify many allowances as variable, not fixed, to respect the cap, complicating structures and adding regulatory scrutiny. Even though the UK removed the cap, RBAs still exist in many packages.

Tension point

If you accelerate legacy variable awards while keeping RBAs at cap‑era levels, total effective liquidity to MRTs could spike and undermine the reform’s intention to pivot value back to risk‑adjustable variable pay. Several law‑firm and regulator summaries emphasise that the policy intent is to rebalance away from fixed components that cannot be risk‑adjusted.

Balancing actions to consider

- Sunset or taper RBAs over one to two cycles as accelerated vesting is implemented, restoring a healthier fixed and variable mix and preserving malus and clawback reach over a larger slice of total remuneration

- Convert RBA value to variable allowances or upfront instruments within the Code, then rely on deferral and instruments to keep risk alignment while improving perceived fairness across cohorts

- Guardrails: keep meaningful retention on upfront instruments (as the PRA continues to expect) and maintain malus and clawback triggers aligned to conduct, risk and financial outcomes

A practical decision matrix for Remuneration Committees

Implementation playbook: how to decide (and defend) your path

Segment and model the MRT population

You should segment and model the MRT population by role/seniority (SMFs vs other MRTs), by legacy plan type and by jurisdiction. Map the unvested pipeline and quantify the cash vs instrument mix and scheduled vesting by quarter through 2029. Stress‑test scenarios: status quo, moderate acceleration, full alignment to new minima, using the revised proportionality threshold. (Regulatory summaries indicate fewer MRTs and higher de minimis thresholds; use this to refine the “who” as well as the “how.”)

Financial capacity and pool planning

Model short‑term liquidity and accounting impacts (including any charge from award modification under your accounting policy), and the effect on future‑year bonus pools under your pool‑setting formula. The policy intent behind removing the cap was to restore variable pay flexibility so firms can absorb losses via variable reductions; avoid locking in future costs.

Risk and accountability overlay

Confirm malus/clawback frameworks remain at least as strong post‑change. Preserve long‑tail clawback for senior roles as appropriate (historic rules envisaged up to seven-to-ten years for SMFs). Document how accelerated schedules still allow ex post risk adjustment if adverse outcomes or risk events emerge.

RBAs strategy

Decide whether RBAs are tapered, re‑characterised, or retained. Tie any acceleration to a fixed‑pay glidepath down (within market constraints) to reflect the shift the regulators envisioned.

Governance, disclosure and fairness

Update the Remuneration Policy Statement (RPS) and committee minutes to show the rationale, stakeholder impacts, and how the approach aligns with safety and soundness. The PRA/FCA reform materials emphasise governance ownership, record‑keeping and clarity of decision‑making.

Manage internal equity: if EU staff can’t accelerate, communicate the regulatory drivers and consider alternative retention tools within EU constraints.

Timing and transition

For calendar‑year firms, you can (subject to plan rules) adopt selected features for 2025 awards and for unvested prior‑year awards, then move wholesale to the new framework from 2026. Several legal updates and the official communications confirm the optional early‑adoption approach.

(The leanings reflect the direction of the PRA/FCA policy intent and widely‑noted market commentary.)

Communications and stakeholder management

Supervisors

Pre‑brief your supervision teams with a succinct paper covering:

- rationale

- quantitative impacts

- risk alignment safeguards

- RBAs plan

- cross‑border coherence

The policy statements and law‑firm analyses highlight heightened governance expectations and documentation standards.

Shareholders

Explain how the changes reduce fixed‑pay creep (a known unintended consequence of the cap) and restore flexibility to adjust remuneration in downturns, a factor explicitly identified by regulators as a benefit of cap removal.

Employees

Be clear that malus/clawback remains effective and that acceleration is not a giveaway but a recalibration within the Code and consistent with international practice.

Special considerations for banks with large MRT populations

When hundreds or thousands of MRTs hold sizeable deferral tails, even modest acceleration can pull forward tens (or hundreds) of millions in cash and shares, squeezing future profit pools and creating budget asymmetry across business lines. To manage this:

- Phase the change: e.g., accelerate only the next scheduled tranche per award year rather than the entire pipeline; or cap the annual acceleration quantum per individual

- Offset with RBA tapering to control total compensation liquidity while improving risk‑adjustability

- Use instruments creatively: more instruments in deferred portions, maintain/introduce minimum post‑vest holding periods for upfront instruments as expected by the PRA

- Apply proportionality: leverage the raised de minimis thresholds and simplified MRT scope to focus heavier structures on genuine risk takers; this was a central theme of the consultation and final policy

Recommended next steps (90‑day plan)

- Diagnostics: complete a full inventory of unvested awards by cohort; map to proposed target schedules consistent with the 4‑year minimum and marginal 60% threshold

- Scenario modelling: build P&L, CET1, share usage and pool impact under three scenarios (no acceleration / limited / full). Stress‑test with downside performance overlays. (Rationale ties to policy objectives around safety and soundness and adaptability of variable pay)

- RBAs policy: define taper/convert strategy and communications. Link to competitive pay narrative post‑cap removal

- Governance pack: draft RemCo paper capturing legal basis (policy statements), fairness, risk alignment, and disclosure plan (RPS update)

- Execution readiness: update plan rules where needed; align payroll, tax, and systems for pro‑rata vesting; confirm malus/clawback mechanics and triggers under the revised timelines

Conclusion

These reforms give UK firms genuine latitude to rebalance pay toward risk‑sensitive variable elements and to simplify remuneration mechanics. Acceleration of legacy deferrals can fit into that agenda, but it should be selective, budget‑aware and coupled with an RBA strategy that prevents total compensation liquidity from ballooning. If you can evidence strong malus/clawback, thoughtful MRT scoping and credible financial capacity, you’ll be well placed to implement the new framework and to defend it to supervisors, shareholders and employees alike.

Sources and further reading

- PRA/FCA remuneration reform policy (final): Bank of England (PRA) PS21/25 & FCA cross‑references—scope, deferral, MRT identification, and implementation timing. [bankofengland.co.uk]

- Bonus cap removal (effective 31 Oct 2023): FCA PS23/15 / PRA PS9/23; aims and rationale. [fca.org.uk], [bankofengland.co.uk]

- Legal analyses of the reforms: A&O Shearman insights (MRT scope; deferral/retention relaxations; implementation options). [aoshearman.com],

- Joint policy summaries: Reed Smith client alert (deferral period, marginal 60% threshold, MRT identification). [reedsmith.com]

- Consultation summaries and timelines: City HR (concise recap of Consultation Paper proposals and timing); Cadwalader overview. [cityhr.co.uk], [cadwalader.com]

- EU baseline for cross‑border comparisons: EBA Guidelines on sound remuneration (CRD V aligned); Skadden note on UK–EU divergence. [eba.europa.eu], [skadden.com]

- Role‑based allowances (historical context): Pinsent Masons on EBA’s RBA stance. [pinsentmasons.com]